By Angelo Meda, Head of Equities at Banor

Chips Cool Down After the AI Rally

Summer has arrived well ahead of schedule. With thermometers seemingly locked above 35°C and air conditioners now promoted to safe-haven assets, it is only natural to wonder whether the record-breaking heat has also spread to financial markets. The answer, at least judging by recent weeks, is a firm “it depends.” While the heat has been constant, stock markets have alternated between scorching days and sudden storms, particularly within the technology sector.

The best analogy is probably this: semiconductors have been like asphalt during the hottest hours of the afternoon. They became so overheated that some investors felt it was time to slow down before their shoes started melting too. After an extraordinary first half of the year, fuelled by the race to invest in artificial intelligence, the chip sector experienced several profit-taking sessions, some of them rather severe. After all, when a sector rises almost uninterrupted for months, it takes only a light breeze—or doubts about valuations—to persuade some investors to lock in profits.

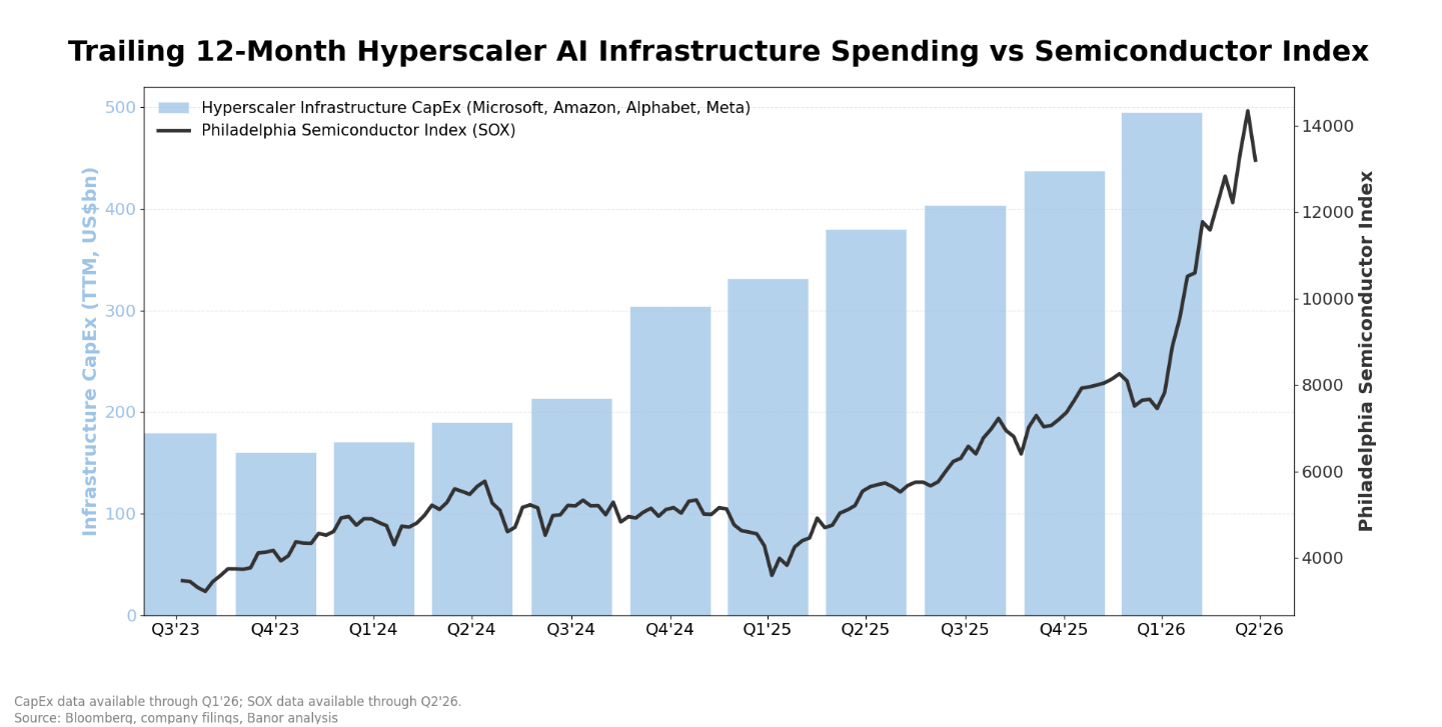

Despite these corrections, the structural investment theme remains intact: demand for high-performance memory, GPUs, HBM (High Bandwidth Memory), and AI infrastructure continues to be one of the strongest drivers of global growth.

The paradox is that just as investors began to wonder whether AI fever had become too intense, corporate earnings reminded everyone that solid fundamentals still underpin the excitement. Guidance from memory manufacturers such as Micron confirmed strong demand and long-term order visibility—factors that are rarely associated with a passing fad. This does not eliminate the risk of volatility, but it suggests that the story is far from over. Rather, we are probably entering a phase in which the market is demanding a bit more pricing discipline. In the coming days, second-quarter corporate results will be released. We are likely to receive further confirmation of how much economic growth is being driven by AI investment, and we may also begin to see some early effects on the profit margins of companies that have already implemented AI technologies.

The paradox is that just as investors began to wonder whether AI fever had become too intense, corporate earnings reminded everyone that solid fundamentals still underpin the excitement. Guidance from memory manufacturers such as Micron confirmed strong demand and long-term order visibility—factors that are rarely associated with a passing fad. This does not eliminate the risk of volatility, but it suggests that the story is far from over. Rather, we are probably entering a phase in which the market is demanding a bit more pricing discipline. In the coming days, second-quarter corporate results will be released. We are likely to receive further confirmation of how much economic growth is being driven by AI investment, and we may also begin to see some early effects on the profit margins of companies that have already implemented AI technologies.

The performance of global equity markets reflects this delicate balance between enthusiasm and caution. In the United States, major indices continue to trade near record highs, supported by an economy that, although gradually slowing, still demonstrates remarkable resilience. At the same time, an increasingly clear sector rotation is underway. In recent sessions, the Dow Jones Industrial Average has continued to reach new highs, while parts of the technology sector—and semiconductors in particular—have taken a well-deserved breather. It serves as a classic reminder that, in financial markets, even the winners occasionally need time to catch their breath.

Europe has also maintained a constructive tone. The prospect of a less restrictive monetary policy compared to recent months, combined with generally orderly macroeconomic data, has enabled investors to look beyond geopolitical and trade-related uncertainties. Concerns about tariffs and tensions in technology supply chains naturally remain unresolved, but for now the prevailing view is that investment in artificial intelligence represents a multi-year cycle rather than a short-lived speculative craze.

In Asia, meanwhile, the heat has been even more intense. South Korea, which has effectively become a global thermometer for the memory-chip industry, experienced swings worthy of a mountain climate, with sharp declines immediately followed by spectacular rebounds in Samsung and SK Hynix shares. More than volatility, it resembled a Finnish sauna applied to stock markets. The explanation, however, remains rational: when an industry grows at exceptional rates, expectations rise just as rapidly, and every piece of news—positive or negative—is amplified.

The overall impression is that the market is undergoing a period of consolidation rather than a reversal. Valuations for many AI-related companies are undoubtedly demanding, making episodes of volatility entirely natural. Nevertheless, the investment trajectory of major cloud providers, data centres, and the broader technology supply chain continues to suggest that semiconductor demand will remain elevated for many years to come. The real challenge will be distinguishing between companies that will genuinely benefit from this cycle and those that have merely learned to include the letters “AI” in every investor presentation.

For portfolio managers, the message remains unchanged. It is appropriate to remain enthusiastic about major structural growth themes, but without forgetting that even the best marathon runner occasionally needs a stop at the refreshment station. In other words, the heat may persist for a long time, but that does not mean it is necessary to keep running under the midday sun.

After all, the market and summer share one characteristic: after days when it seems impossible to endure even one more degree of heat, a sudden storm is enough to remind us that the perfect temperature does not exist. The same applies to the weather, to semiconductor valuations, and—above all—to investors, who occasionally discover that even chips need time to cool down.

This communication is issued by Banor Capital Limited which is authorised and regulated by the Financial Conduct Authority (FRN: 523080). For Professional Clients and Eligible Counterparties only. Not for Retail clients. The content is for information purposes only and does not constitute investment advice, a recommendation, or an offer/solicitation to buy or sell any investment. Views are those of the speaker and may change. Any views expressed regarding future market conditions, sector performance, or investment returns are forward-looking statements and may not materialise. Actual outcomes may differ materially. Forecasts are not a reliable indicator of future performance. This communication is not directed to any person in any jurisdiction where doing so would be unlawful; distribution may be restricted.

Angelo Meda is Head of Equities at Banor SIM S.p.A. and provides research and advisory input to Banor Capital Ltd pursuant to an advisory agreement.

This article is an English translation of an article originally prepared and published by Banor SIM.