By Angelo Meda, Head of Equities at Banor

Buybacks on pause: a push for growth or turbulence?

Aircraft are designed with redundancy: one functioning engine guarantees the necessary thrust, flight control, and power for the instruments, allowing the aircraft to continue flying or to land at a nearby airport. ETOPS certification (Extended-range Twin-engine Operations Performance Standards) ensures that an aircraft can cover long oceanic distances even with only one engine operating. Replacing older three- or four-engine aircraft used for long-haul routes with cheaper and more reliable twin-engine planes has revolutionized the aviation industry.

Financial markets do not have built in redundancy, but in general they do have propulsion mechanisms that drive global equity markets: earnings growth, dividends, buybacks, and multiple expansion. The first three, which are clear and measurable, have so far supported the market, while the last is more uncertain. In theory it depends on variables such as interest rates and inflation, but in reality it is also strongly linked to psychology and investor sentiment.

We are now, however, in a phase where one of these engines seems to be losing thrust—or even shutting down—for some companies with significant weight in the indices: buybacks. We are not referring to the weeks prior to earnings releases, when US regulations require companies to suspend share repurchases to prevent accusations of insider trading or the sending of potentially misleading signals to investors.

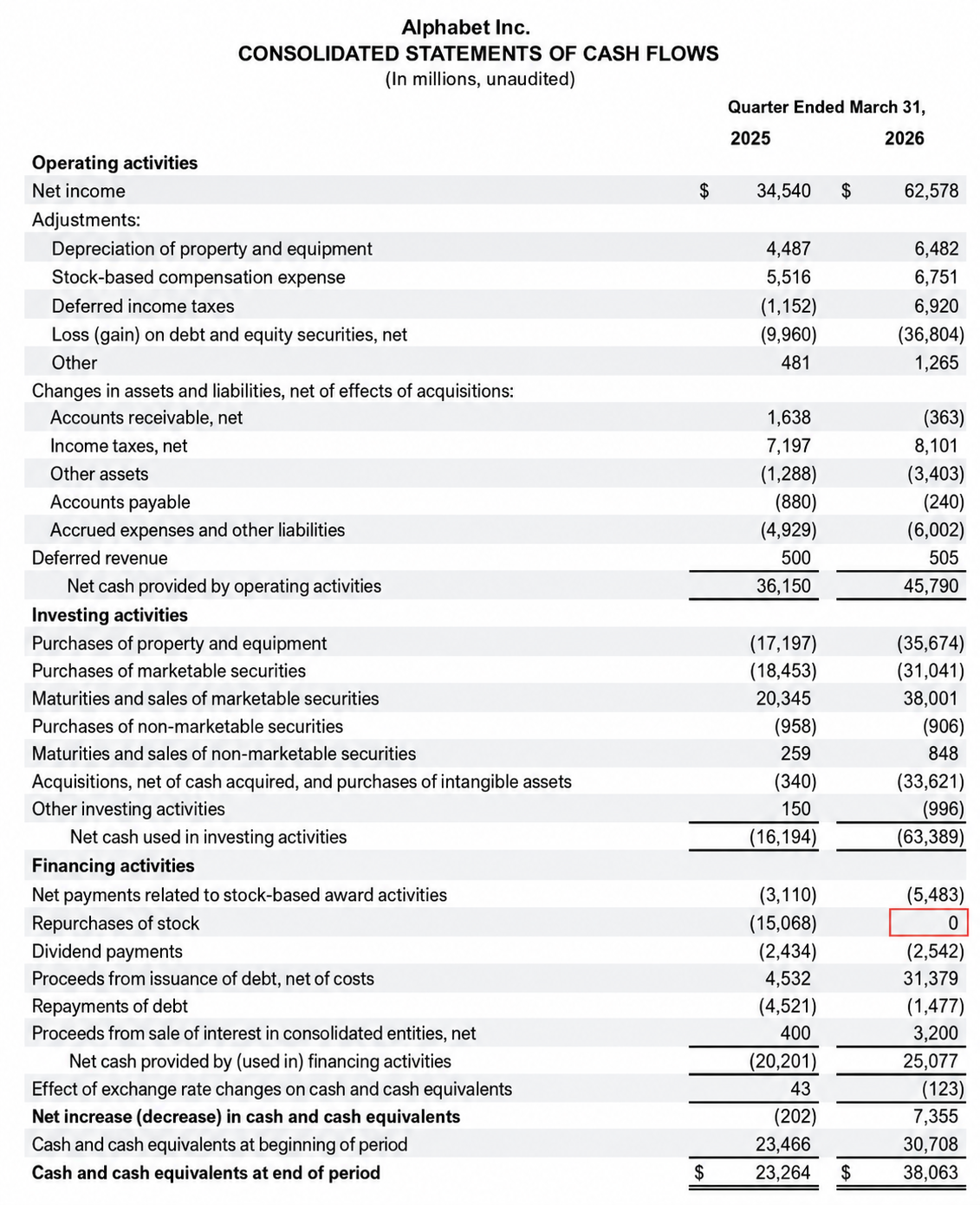

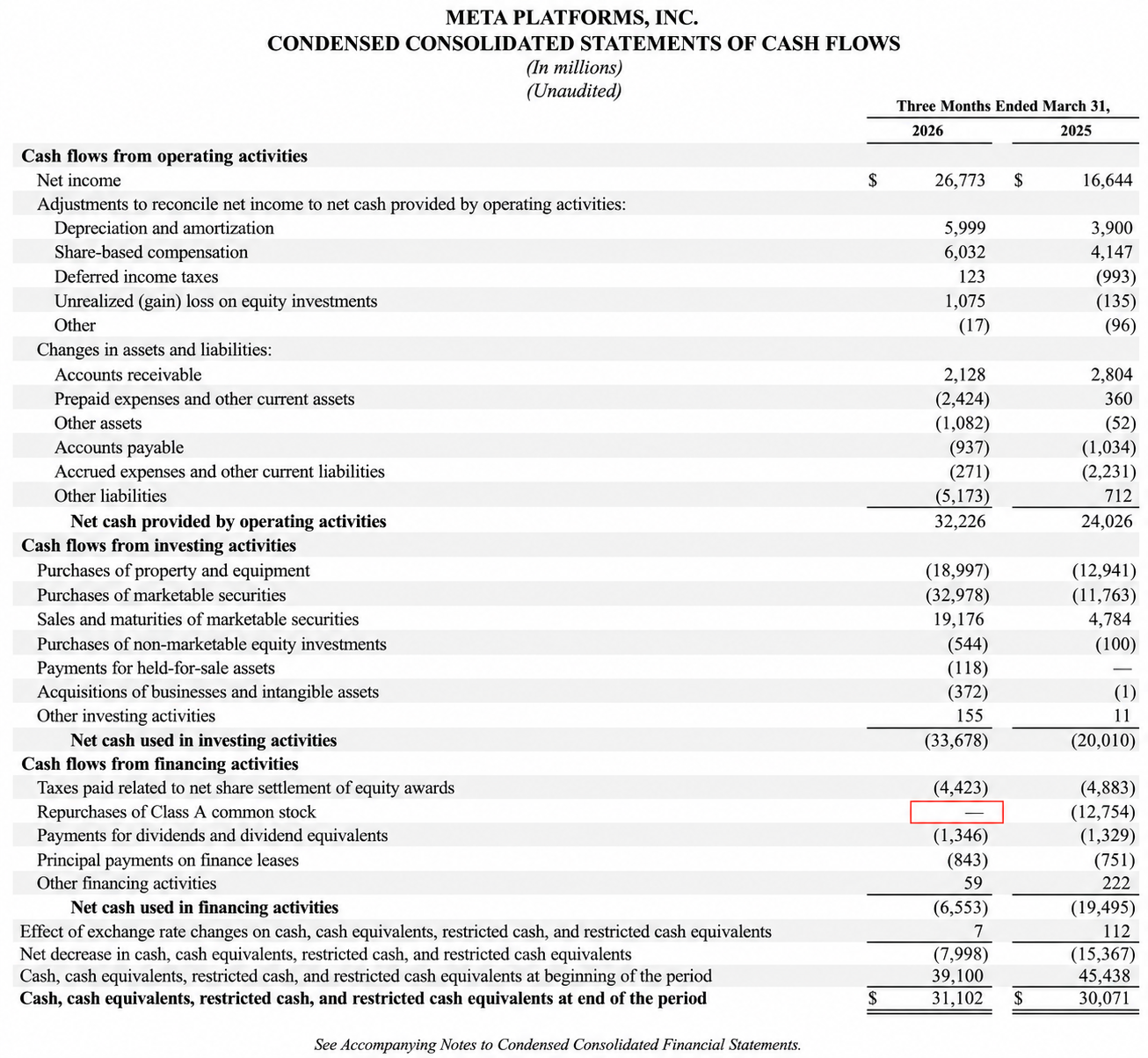

If we look at the first-quarter 2026 cash flow statements of two companies that reported earnings at the end of April, Meta and Alphabet, the line item “Repurchases of stock” is zero for both. A year ago, they had spent $12 billion and $15 billion respectively.

This means there is no longer excess cash available to return to shareholders and, unwilling to materially increase gross debt, companies are forced to cut the simplest form of discretionary spending—buybacks.

What does this imply for company valuations? It is difficult to say, but we can make two observations.

The first is that if companies continue to use shares as part of employee and executive compensation (stock based compensation), then each year, instead of buybacks having a positive impact on earnings per share growth, the effect will be negative. To give a sense of scale, stock based compensation at Alphabet accounted for almost 10% of total costs in the first quarter of 2026.

The second is that over the long term, the market will evaluate the return on these investments. If a company, instead of buying back its own shares, invests in machinery, research and development, or acquisitions that generate a return above the cost of capital, it will by definition create value. To date, hyperscalers have invested around $1.5 trillion and are expected to exceed $2 trillion by the end of the year. If, for example, we assume a cost of capital of 10%, this implies generating roughly $200 billion per year in additional operating profit—essentially creating a new Google in a relatively short period of time.

For now, therefore, the market resembles an aircraft flying with one engine out: it can still stay aloft, but with reduced range, and soon it will be necessary to assess the returns on these investments or see whether other sectors resume providing thrust. In the meantime, we stay on course, but should expect a slowdown and some turbulence.

This communication is issued by Banor Capital Limited which is authorised and regulated by the Financial Conduct Authority (FRN: 523080). For Professional Clients and Eligible Counterparties only. Not for Retail clients. The content is for information purposes only and does not constitute investment advice, a recommendation, or an offer/solicitation to buy or sell any investment. Views are those of the speaker and may change. Any views expressed regarding future market conditions, sector performance, or investment returns are forward-looking statements and may not materialise. Actual outcomes may differ materially. Forecasts are not a reliable indicator of future performance. This communication is not directed to any person in any jurisdiction where doing so would be unlawful; distribution may be restricted.

Angelo Meda is Head of Equities at Banor SIM S.p.A. and provides research and advisory input to Banor Capital Ltd pursuant to an advisory agreement.

This article is an English translation of an article originally prepared and published by Banor SIM.